Report on Investment Performance for the fiscal year ending June 30, 2017

The market value of University of Rochester Long-Term Investment Pool (“LTIP”) as of June 30, 2017 was $2.3 billion. Performance for the year was 14.3%, net of all fees and expenses, compared with the benchmark return of 14.8%. Performance of the LTIP has exceeded the benchmark, net annualized, for three, five, and ten year periods. Ten year LTIP performance of 5.3% net annualized is 1.0% above the 4.3% annual return on the benchmark. While this result is below the expected 8% long-term return from the LTIP, outperformance versus the benchmark is significant.

Asset Allocation and Performance

The chart below shows asset allocation targets and ranges (“policy portfolio”) compared to actual allocations on June 30, 2017.

*6/30/17 values and performance preliminary, unaudited and subject to change.

**Committee approval in September 2016, effective until December 31, 2017. May not foot due to rounding

| Target | Actual* | + / – | Range** | ||

| Traditional Investments Consisting of: | |||||

| Total, Publicly-traded long equities | 35 | 36 | 1 | 34 – 36 | |

| Fixed Income | 3 | 3 | 0 | 3 – 3 | |

| Cash (not held by managers) | 4 | 4 | 0 | (2) – 6 | |

| Total, Traditional Investments | 42 | 43 | 1 | 35 – 45 | |

| Alternative Investments Consisting of: | |||||

| Hedge Funds | 25 | 26 | 1 | 25-28 | |

| Private Equity / Distressed | 22 | 20 | (2) | 19 – 23 | |

| Real Assets | 11 | 11 | 0 | 11 – 14 | |

| Total, Traditional Investments | 58 | 57 | (1) | 55 – 65 | |

| TOTAL | 100 | 100 | (0) | 100 | |

The LTIP’s 57% alternative investment allocation consists of hedge funds and partnerships investing in real assets and equities of private companies. This allocation is near the mean allocation to alternatives of the largest educational endowments. The net average annualized ten year return of 6.1% per annum from the LTIP’s alternative program exceeded the return on the LTIP, with significantly lower volatility (alternative volatility was 4.4% for the ten years ending June 30, 2017, compared to 7.2% volatility for the LTIP). Importantly, the LTIP’s alternative investments generate attractive returns in periods of weak or negative performance by public equities and bonds.

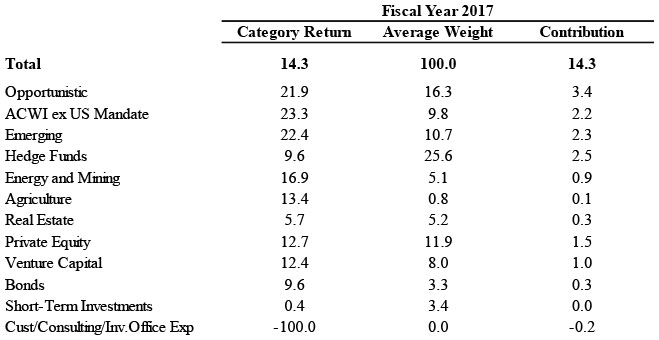

Comment on Asset Category Performance

The weights and contributions to return for asset classes as of June 30, 2017 are shown in chart below.

Public Equities

The publicly-traded equity portfolio (Opportunistic, ACWI ex-U.S., and Emerging) represented 36% of the total portfolio, above the target allocation of 35%. The publicly-traded equity portfolio returned 22.4% net for the fiscal year, above the 18.8% return for the MSCI All Country World Index (“ACWI”). The publicly-traded equity portfolio also outperformed the benchmark for the three, five, and ten year time periods.

Opportunistic funds represented 15% of the LTIP at the end of June. The group returned 21.9% net for the fiscal year, above the 18.8% return for the ACWI. The group also outperformed the ACWI for the three, five and ten year time periods.

International equity represented 21% of the LTIP at the end of June. Performance for the fiscal year was 22.9% net, above the 20.5% return of the benchmark, the ACWI ex-U.S. The group also outperformed the benchmark for the three, five, and ten year time periods. Emerging markets, which represented slightly more than half of the international public equity allocation, returned 22.4% net for the fiscal year, slightly underperforming the 23.7% return of the benchmark, the MSCI Emerging Markets Index. For all longer periods, the emerging group outperformed the Index.

Hedge Funds

The hedge fund allocation was 26% at the end of June, slightly above the target allocation of 25%. The hedge fund portfolio’s net return was 9.6% for the fiscal year. Equity-oriented managers returned 9.6% net, diversifiers returned 9.0% net, and the liquid diversifier manager returned 12.2% net. The hedge fund ten-year net annualized return was 4.8%, above the 4.3% return of the LTIP benchmark. The ability of hedge funds to deliver returns comparable to those of the overall LTIP with lower volatility has been a key component of the LTIP’s attractive long-term risk-adjusted return profile.

Real Assets

Partnerships investing in real assets (Energy and Mining, Agriculture, and Real Estate) represented 11% of the LTIP at the end of June, at the target and lower limit in the allocation range. The real assets portfolio returned 11.2% net for the fiscal year. The net annual return of 3.1% for the most recent five year period and ten year net annual return of 0.7% are disappointing. Ten year results were impacted by the global financial crisis as well the decline in energy prices. Real assets do however serve an important role in the LTIP by stabilizing performance during periods of volatility in public markets.

The LTIP’s real asset partnerships invest in energy/mining and real estate/agriculture. Energy and mining, a 6% allocation within the LTIP, returned 16.9% net for the fiscal year. The ten year net annualized return for energy and mining was -2.0%. Real estate and agriculture, a 5% allocation within the LTIP, returned 6.2% net for the fiscal year. The ten year net annualized returns for real estate and agriculture were below expectations at 2.1% and 4.3%, respectively, primarily as a result of the global financial crisis.

Private Equity

The LTIP’s private equity portfolio consists of partnerships investing in buyouts/growth, distressed/credit, and venture capital, and represented 20% of the LTIP at the end of the fiscal year, below the target allocation of 22%. Private equity returned 12.6% net for the fiscal year; the ten year net annualized return was 12.0%. The LTIP’s private equity managers continued to distribute cash and marketable securities at a steady pace through sales of portfolio companies to strategic buyers and by initial public offerings.

Buyouts, the largest strategy allocation within private equity at 10%, returned 14.4% net for the fiscal year. Venture capital, representing 8% of the LTIP, returned 12.4% net for the fiscal year. Distressed, a 2% allocation within the LTIP, returned 5.7% net for the fiscal year. Ten year annualized net returns for these subcategories were 10.5%, 15.6% and 10.4%, respectively.

Fixed Income

The allocation to fixed income and cash equivalents represented 7% of the LTIP. For the fiscal year, the LTIP’s fixed income and cash investments returned 4.9% net, compared to 0.1% for the blended bond/cash index. The ten year annualized return for fixed income was 4.3%, compared to the return of 4.5% for the index.

Liquidity

The LTIP has ample liquidity, with 63% of assets convertible into cash within one year.

Report on Investment Performance for the fiscal year ending June 30, 2017

The market value of University of Rochester Long-Term Investment Pool (“LTIP”) as of June 30, 2017 was $2.3 billion. Performance for the year was 14.3%, net of all fees and expenses, compared with the benchmark return of 14.8%. Performance of the LTIP has exceeded the benchmark, net annualized, for three, five, and ten year periods. Ten year LTIP performance of 5.3% net annualized is 1.0% above the 4.3% annual return on the benchmark. While this result is below the expected 8% long-term return from the LTIP, outperformance versus the benchmark is significant.

Asset Allocation and Performance

The chart below shows asset allocation targets and ranges (“policy portfolio”) compared to actual allocations on June 30, 2017.

*6/30/17 values and performance preliminary, unaudited and subject to change.

**Committee approval in September 2016, effective until December 31, 2017. May not foot due to rounding

**Committee approval in September 2016, effective until December 31, 2017. May not foot due to rounding

| Target | Actual* | + / – | Range** | ||

| Traditional Investments Consisting of: | |||||

| Total, Publicly-traded long equities | 35 | 36 | 1 | 34 – 36 | |

| Fixed Income | 3 | 3 | 0 | 3 – 3 | |

| Cash (not held by managers) | 4 | 4 | 0 | (2) – 6 | |

| Total, Traditional Investments | 42 | 43 | 1 | 35 – 45 | |

| Alternative Investments Consisting of: | |||||

| Hedge Funds | 25 | 26 | 1 | 25-28 | |

| Private Equity / Distressed | 22 | 20 | (2) | 19 – 23 | |

| Real Assets | 11 | 11 | 0 | 11 – 14 | |

| Total, Traditional Investments | 58 | 57 | (1) | 55 – 65 | |

| TOTAL | 100 | 100 | (0) | 100 | |

The LTIP’s 57% alternative investment allocation consists of hedge funds and partnerships investing in real assets and equities of private companies. This allocation is near the mean allocation to alternatives of the largest educational endowments. The net average annualized ten year return of 6.1% per annum from the LTIP’s alternative program exceeded the return on the LTIP, with significantly lower volatility (alternative volatility was 4.4% for the ten years ending June 30, 2017, compared to 7.2% volatility for the LTIP). Importantly, the LTIP’s alternative investments generate attractive returns in periods of weak or negative performance by public equities and bonds.

Comment on Asset Category Performance

The weights and contributions to return for asset classes as of June 30, 2017 are shown in chart below.

Public Equities

The publicly-traded equity portfolio (Opportunistic, ACWI ex-U.S., and Emerging) represented 36% of the total portfolio, above the target allocation of 35%. The publicly-traded equity portfolio returned 22.4% net for the fiscal year, above the 18.8% return for the MSCI All Country World Index (“ACWI”). The publicly-traded equity portfolio also outperformed the benchmark for the three, five, and ten year time periods.

Opportunistic funds represented 15% of the LTIP at the end of June. The group returned 21.9% net for the fiscal year, above the 18.8% return for the ACWI. The group also outperformed the ACWI for the three, five and ten year time periods.

International equity represented 21% of the LTIP at the end of June. Performance for the fiscal year was 22.9% net, above the 20.5% return of the benchmark, the ACWI ex-U.S. The group also outperformed the benchmark for the three, five, and ten year time periods. Emerging markets, which represented slightly more than half of the international public equity allocation, returned 22.4% net for the fiscal year, slightly underperforming the 23.7% return of the benchmark, the MSCI Emerging Markets Index. For all longer periods, the emerging group outperformed the Index.

Hedge Funds

The hedge fund allocation was 26% at the end of June, slightly above the target allocation of 25%. The hedge fund portfolio’s net return was 9.6% for the fiscal year. Equity-oriented managers returned 9.6% net, diversifiers returned 9.0% net, and the liquid diversifier manager returned 12.2% net. The hedge fund ten-year net annualized return was 4.8%, above the 4.3% return of the LTIP benchmark. The ability of hedge funds to deliver returns comparable to those of the overall LTIP with lower volatility has been a key component of the LTIP’s attractive long-term risk-adjusted return profile.

Real Assets

Partnerships investing in real assets (Energy and Mining, Agriculture, and Real Estate) represented 11% of the LTIP at the end of June, at the target and lower limit in the allocation range. The real assets portfolio returned 11.2% net for the fiscal year. The net annual return of 3.1% for the most recent five year period and ten year net annual return of 0.7% are disappointing. Ten year results were impacted by the global financial crisis as well the decline in energy prices. Real assets do however serve an important role in the LTIP by stabilizing performance during periods of volatility in public markets.

The LTIP’s real asset partnerships invest in energy/mining and real estate/agriculture. Energy and mining, a 6% allocation within the LTIP, returned 16.9% net for the fiscal year. The ten year net annualized return for energy and mining was -2.0%. Real estate and agriculture, a 5% allocation within the LTIP, returned 6.2% net for the fiscal year. The ten year net annualized returns for real estate and agriculture were below expectations at 2.1% and 4.3%, respectively, primarily as a result of the global financial crisis.

Private Equity

The LTIP’s private equity portfolio consists of partnerships investing in buyouts/growth, distressed/credit, and venture capital, and represented 20% of the LTIP at the end of the fiscal year, below the target allocation of 22%. Private equity returned 12.6% net for the fiscal year; the ten year net annualized return was 12.0%. The LTIP’s private equity managers continued to distribute cash and marketable securities at a steady pace through sales of portfolio companies to strategic buyers and by initial public offerings.

Buyouts, the largest strategy allocation within private equity at 10%, returned 14.4% net for the fiscal year. Venture capital, representing 8% of the LTIP, returned 12.4% net for the fiscal year. Distressed, a 2% allocation within the LTIP, returned 5.7% net for the fiscal year. Ten year annualized net returns for these subcategories were 10.5%, 15.6% and 10.4%, respectively.

Fixed Income

The allocation to fixed income and cash equivalents represented 7% of the LTIP. For the fiscal year, the LTIP’s fixed income and cash investments returned 4.9% net, compared to 0.1% for the blended bond/cash index. The ten year annualized return for fixed income was 4.3%, compared to the return of 4.5% for the index.

Liquidity

The LTIP has ample liquidity, with 63% of assets convertible into cash within one year.